Metro-east schools file tax levy requests: The complicated math behind your bill

Metro-east school districts recently submitted their property tax levy requests to their county clerks.

How much of your property taxes will go toward your local school? The answer is complex, but these levy requests play a role in determining how much residents will ultimately owe next year.

The levy is the amount of tax revenue the schools intend to collect from property owners in their districts. Levy requests, at this point, are preliminary. The actual amount of property taxes payable in 2026 will be determined later in the tax cycle.

There are several key factors that influence your tax bill.

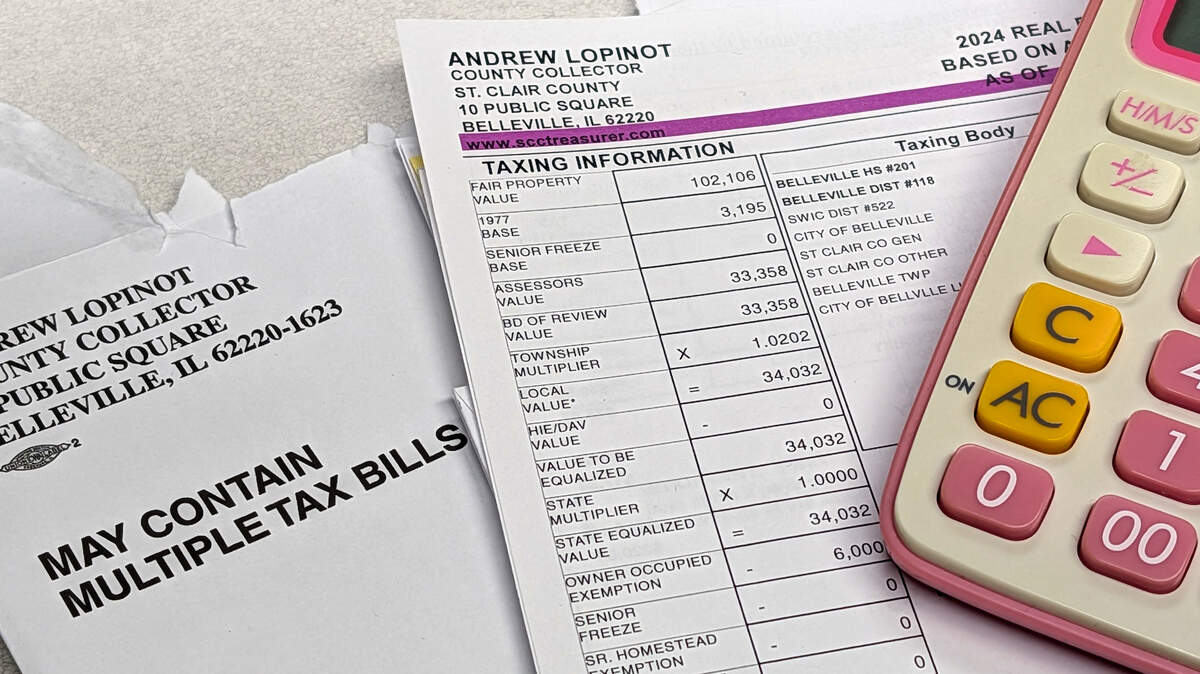

The first is the assessed value of your home, which generally equals about one-third of its market value. This figure, along with exemptions and other adjustments, is used to calculate the taxable value of your property.

As housing prices have risen throughout much of the metro-east, the total taxable value of property in these school districts is expected to increase as well. This is known as the equalized assessed valuation, or EAV.

Each taxing body has its own rate—a percentage multiplied by your taxable value to determine how much goes to that entity. The rate is calculated by dividing the final levy by the EAV, then multiplying by 100.

For example, if your home’s market value is $200,000, its taxable value is likely about $60,000. If your school district’s rate is 4 percent, then $4 for every $100 of taxable value—a total of $2,400—would go to the district.

Specifics such as EAV and the tax rate are not yet determined. Other factors may vary based on each taxpayer’s situation. As a result, it is too early to accurately estimate your bill.

“Each parcel has its own story,” said Dina Thurlow, chief deputy clerk for St. Clair County.

Proposed levies in a ‘backwards’ system

The timing of the Illinois property tax cycle makes it difficult for both homeowners and school districts to estimate bills and set levy requests.

Districts must submit levy requests to the county each December—months before they know the final EAV. County clerks provide EAV estimates, but the final EAV isn’t set until spring.

“This is where we’re backwards all day long,” said Matt Stines, superintendent of Grant Community Consolidated School District 110 in Fairview Heights.

The EAV is key. The higher the EAV, the more a district can request in its levy without increasing the tax rate. If home values increase, taxpayers in that district may see a higher bill even if their rate remains steady or decreases.

Districts often aim to avoid large rate swings. They use EAV projections to estimate where the tax rate might end up. If the EAV comes in higher than the estimate, the district’s final rate will be lower than projected. If the EAV is lower, the final tax rate will likely be higher.

After a district submits its request, the county clerk calculates and provides the EAV to the district and verifies each fund in the levy does not exceed any maximum tax rate cap set by law or voters.

Generally, a district cannot request a higher levy than was submitted in December, but can still reduce or abate the levy at this stage.

Because the tax rate depends on the EAV—not just the levy—a district requesting a higher levy than it extended (received if there were 100 percent billing/collections) the prior year does not automatically mean tax bills will rise. Take Millstadt Consolidated Community School District 160. The district seeks to levy $8,644,521 for tax year 2025, more than $400,000 above the previous year’s extension. Yet if EAV grows as projected, the tax rate will actually be lower than last year.

If your taxable home value stays steady, under these projections you’d pay about $2.69 for every $100 of taxable value. Last year, the rate was $2.78 for every $100. “An increase in money (requested) does not necessarily equate to an increase in rate,” Millstadt Superintendent Brian Mentzer said.

Levy high, abate later

Since districts can seldom increase levy requests after submission, some this winter based their requests on a higher EAV than they expect, knowing they may abate later so residents will be billed less than originally requested.

“We over-inflate to capitalize on what we can, but we also abate to keep the tax rate low,” Mascoutah School District 19 Superintendent David Deets said.

Mascoutah intentionally overestimated EAV and submitted a levy request of about $19.9 million, which is about 23 percent higher than the previous tax year’s extension.

Recent board action shows how quickly these figures can shift. The district abated $1.7 million for bonds—a figure not reflected in the levy request, Deets said. With this abatement, the projected rate is lower and the increase from tax year 2024 to 2025 is less pronounced.

Because the final EAV released in spring will likely differ from early projections, the tax rate may change once again. Further abatements in the spring may alter the rate a final time.

Grant Community Consolidated School District 110 in Fairview Heights uses a similar strategy: levy high to capture available funds, knowing abatements can reduce taxpayers’ burden. In their case, Stines said the district might see an atypical EAV increase—but probably not as much as the EAV used for levy calculations—as the city retires a tax increment financing district, or TIF. TIFs lower EAV for taxing bodies they overlap.

There’s no ‘right or wrong’ approach, superintendents say

Districts sometimes follow other philosophies in setting levies, and there is no one "right or wrong" approach, Deets said. “There are different philosophies of how to get those numbers from every person who sits in this chair,” said Harmony-Emge School District 175 Superintendent Dustin Nail.

Mentzer, who helped craft Millstadt’s levy and oversaw District 201 levies for 14 years, said he tries to set the December levy based on the best available EAV projections.

Boards may later decide to abate taxes after learning the final EAV and its effect on rates. For example, if the EAV does not rise as projected, the district can abate in the spring to keep the rate steady.

Nail said Harmony-Emge uses historical data to project EAV when setting its request.

His district takes a needs-based approach—requesting what is necessary to operate schools, not necessarily the maximum allowed.

To keep tax rates steady or even reduce them while still collecting necessary dollars, Nail said the district adjusts the amounts levied in each fund, maximizing fund rates only as needed.

“We owe it to our taxpayers to make sure the burden doesn’t become too much for them,” Nail said. At the same time, he said, his primary responsibility is ensuring schools have the resources needed to serve students.